A model portfolio—along with a sober assessment of future returns.

Retirement

getty

Whew. If you didn’t panic and sell, your portfolio has recovered from the pandemi-crash. Now you can look forward to a rich retirement.

Somewhat rich. You’re going to be earning a 2% annual return on your savings. That return, which is after inflation and before taxes, is perhaps less than you were figuring on. It’s a forecast of what will happen to investors over the next 20 years.

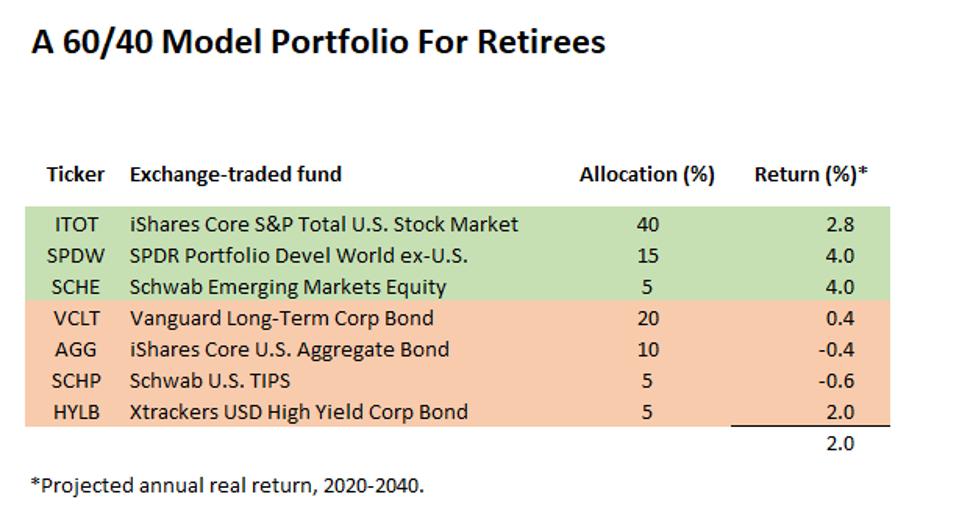

Below you will find a model portfolio: a recommended list of seven cost-efficient funds that will put 60% of your money in U.S. and foreign stocks and 40% in different kinds of bonds.

The 2% forecast is no more than a hunch, since no one knows what the future will bring, but I’ll justify it by citing the work of three Wall Street firms that make return forecasts: BlackRock

BLK

A year ago, in my last round of futurism, I had 2.5% as the expected long-term rate of return on a 60/40 portfolio mixing stocks and bonds. The number is lower now for a simple reason: Stocks and bonds have gotten more expensive. A dollar you put into them gets you less earnings or interest.

The bull market is great for a retiree who is selling securities just at the moment, but it’s bad news for a younger person buying them. The money that a 50-year-old puts into a 401(k) now will grow by only 49% in spending power by the start of a retirement at age 70.

My forecast for real returns is built on assumptions about what’s in store for five things: inflation, U.S. stocks, foreign stocks, high-quality bonds and junk bonds.

Inflation

Nominal returns don’t do anything for your retirement. You need spending power. So you need to build an estimate of future inflation into your planning.

The experts project inflation rates in the neighborhood of 2%. BlackRock Investment Institute, the research arm of the giant money manager, foresees a price surge down the road, with inflation averaging 2.8% over 2025-2030. Research Affiliates, best known for running index funds weighted by fundamentals like earnings rather than by market capitalization, estimates 2.2% annually over the next decade. GMO, an institutional money manager with a value bent, has the same 2.2% expectation over seven years.

The bond market is a little less pessimistic. Compare yields on nominal Treasury bonds with those on inflation-protected Treasuries (TIPS) and you get a breakeven inflation rate of just over 1.7%. Breakeven means that, if inflation averages 1.7%, the conventional Treasuries and the TIPS will deliver the same result.

But I think the breakeven number needs an adjustment. It probably has a risk premium built into it, meaning that buyers of the nominal bonds are being compensated for bearing uncertainty about what’s going to happen to the price level. So I haircut the breakeven rate to arrive at 1.6% for what market participants implicitly project for inflation. That 1.6% is my forecast.

Before or during your retirement, of course, inflation could be a lot worse. And what is the saver to do about this? You can buy insurance against runaway inflation by owning TIPS, but this insurance is very expensive. Yields on these real-return bonds are negative. I recommend only a small dose of this safety valve. Go all in for TIPS if you crave safety and are willing to lock in a rotten return.

The other way to cope with the cost of living is to own equities and junk bonds. They have a fighting chance of beating inflation over a long investing horizon. But there’s nothing guaranteed about either their returns or their ability to serve as an inflation antidote.

Stocks

U.S. stocks have averaged a total real return (appreciation plus dividends minus inflation) of better than 6% over the past half century. With stock prices now abnormally high in relation to earnings, the future is not likely to be so prosperous for possessors of shares.

The BlackRock affiliate makes predictions about nominal returns that translate into a real return of roughly 5% a year over the next 20 years. This doesn’t sound great but it is, in fact, a bullish view. It’s also a mainstream view. You would scarcely expect an institution supervising $7 trillion to be telling its clients, “Sell all!”

Research Affiliates, more in a position to stick its neck out, forecasts a miserable 0.2% a year (real) for large U.S. stocks over the next decade and 1.9% for small stocks. GMO sees, over a shorter horizon (2020-2027), annual returns of -6.5% for large stocks and -4.5% for small.

I arrive at a 2.8% forecast, midway between the pessimistic RA number and the cheery BlackRock number.

My estimate comes from the earnings yield on the S&P 500. S&P calculates index earnings of $139 for 2019 and an estimated $87 in 2020 and $143 in 2021. While the current-year number is depressed by a recession, the one for next year is inflated by the habitual optimism of stock analysts. So it’s fair to just average these three. Divide the $123 average by the index price today and you get an earnings yield of 3.7%.

You could use a higher number than $123 for long-term earning power, such as the wished-for $143 for next year. But I think that would be too optimistic. You can’t brush 2020 aside. There will be recessions, not just this year but sometime again before the 20 years are up, and they damage stockholders.

Now we’ll translate that 3.7% yield into a return forecast for equities.

If corporations could hypothetically distribute all their earnings and still keep earnings constant in real terms, the 3.7% would be a good guess for future returns from stocks. Alas, corporations have to run pretty fast to keep in place: A good chunk of earnings must be reinvested to maintain a constant earning power. That phenomenon knocks roughly a percentage point off stock returns. (For the arithmetic, see Why High Stock Prices Are Bad For Future Retirees.)

Subtracting 1% for running in place, I get 2.7% for the expected real return on the big-company S&P 500.

Small companies could do better than that; all three of my experts find them depressed and due for outperformance. The full stock market, which blends a large amount of big company capitalization with a smaller dose of small, should be good for a 2.8% return. You’ll see that figure in the model portfolio.

Foreign stocks

Overseas equity markets are cheap, at least compared to the U.S. one. That is to say, their price/earnings ratios are low and their earnings yields correspondingly higher. With higher earnings yields they can deliver more to investors.

To some degree the bearish price/earnings multiples are justified. Europe suffers from a lack of imagination; you don’t see an Amazon or Alibaba there. Emerging markets suffer from a lack of property rights; shareholders can be shortchanged.

Still, the lagging P/Es of foreign markets are probably overdone. All three experts expect foreign stocks to beat their U.S. counterparts, by between 1 and 6 percentage points annually. My view? A compromise. I’ve got both the emerging and the developed foreign markets down for a 4% real return rate.

High-quality bonds

The past year has been terrific for bondholders who bought a while ago and were handed a nice price gain as interest rates declined. For someone investing today, though, the situation is grim.

Today’s buyer of Treasury debt will get no more yield to maturity than 1.5%, not even enough to cover inflation. Inflation-protected Treasuries don’t solve the problem. As noted above, they have negative yields. (How’s that for the patriotic saver? A guaranteed loss.)

High-grade corporate bonds, containing a little risk, offer some prospect for coming out ahead. Although both RA and GMO expect negative real returns over the next seven to ten years, BlackRock sees a positive result for the 20-year investor in corporates. My view is again in the middle. I expect the category to eke out a 0.4% real annual return.

Low-quality bonds

Junk has a lot more risk but pays you pretty well for taking that risk. RA forecasts a 0.8% real return rate over the decade. GMO is silent. BlackRock puts junk down for enough nominal return to likely deliver better than 3% net of inflation. My estimate is in the middle: a 2% real return.

The table displays a 60/40 stock/bond portfolio suitable for a retirement saver willing to take moderate risk. It uses exchange-traded funds because those are available in any brokerage account. But if you happen to bank at Fidelity you can do even better: Much of your money can go into Fidelity open-end index funds for bonds, U.S. stocks and international stocks with rock-bottom expense ratios.

What will you get out of the blended portfolio over the next 20 years? A 2% annual return, I wager. You can be pleasantly surprised if you do better. But it would be foolish to count on doing better.

Retirement portfolio

Forbes

There are, in fact, a lot of cost-efficient ETFs that work here. You can get a fuller look by going to our Best Buy survey:

Guide to Stock Index Funds: 97 Best Buys

BBY

Guide to Foreign Stock Funds: 79 Best Buys

Guide to Investment-Grade Bond Funds: Best Buys

Guide to High-Yield Bond Funds: 20 Best Buys