Opening a new business takes planning, time, money and passion.

PeopleImages | E+ | Getty Images

If you’re your own boss, chances are you aren’t doing enough to save for retirement.

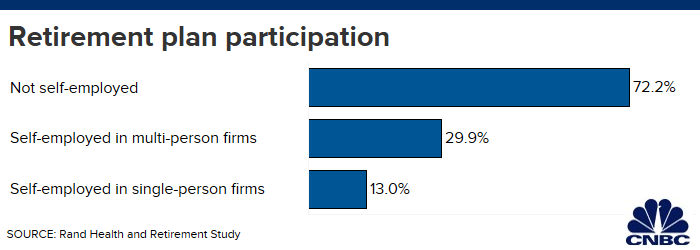

Just over 1 in 10 of self-employed individuals in a single-person business is currently participating in a workplace retirement plan, according to data from The Pew Charitable Trusts.

In comparison, 72% of employees in larger companies utilized a 401(k) at work, the organization found.

Pew studied a total of 4,269 workers aged 50 to 64 in 2012 and 2014. The self-employed participants were divided into solo and multi-person firms.

Entrepreneurs get so wrapped up in the day-to-day running of their businesses that retirement planning often takes a back seat — until the IRS comes looking for its share.

“That very first tax bill is what spurs them to set up a retirement plan,” said Kelley Long, a CPA and member of the American Institute of CPAs’ consumer financial education advocates.

That’s because entrepreneurs may be able to claim a tax credit for the cost of setting up a plan at work.

“Your CPA will say that this is what you owe, and they’ll suggest from the outset that they set up a SEP IRA [simplified employee pension individual retirement account] or a solo 401(k),” she said.

Low balances, higher risk

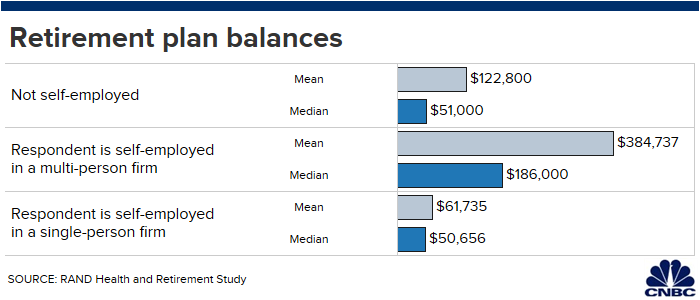

Among workers who had retirement plans at their current jobs, self-employed individuals running solo companies had an average balance of $61,735 saved, versus traditional workers’ mean balance of $122,800.

Business owners with multi-person firms had the highest account balances, with a mean value of $384,737. They also tended to work the most hours and earn the highest wages.

“It is possible that lawyers, doctors, engineers, architects or other ‘knowledge professions’ predominate in this group,” Pew said in its study.

Further, entrepreneurs going solo also tended to make less money. They had median weekly wages of $543.47, according to Pew. Meanwhile, traditional employees had median weekly wages of $920.

Entrepreneurs with multiple workers fared best: They earned a median of $1,200 a week.

Kick off a plan

Luca Sage | Getty Images

Independent workers miss out on the “nudges” about retirement saving that 9-to-5 employees get at work, including automatic enrollment into a 401(k) plan and automatic escalation of workers’ contributions.

That means the burden of selecting the right retirement plan and dutifully saving in it is entirely up to the entrepreneur.

“For the everyday Joe with a gig-economy job, you can narrow it down to the SEP IRA or the solo 401(k),” said Aaron Pottichen, senior vice president of Alliant Retirement Consulting in Austin.

“You have to understand the differences between the two and how much you can afford to save,” he said.

Work with your CPA or financial advisor to determine which is right for you. Here are a few features of the SEP IRA and the solo 401(k).

Solo 401(k). Entrepreneurs wear two hats in the eyes of the IRS when it comes to retirement savings: They are both employers and employees.

As a result, they can contribute up to $56,000 to the retirement plan.

Here’s how: They can make employee deferrals of up to $19,000, plus $6,000 if they’re 50 and over. These entrepreneurs can also make employer contributions to the plan, based on their net self-employment income.

Business owners with a solo 401(k) can also add a Roth option.

More from Personal Finance:

Your Social Security checks could get bigger next year

Denied from public service loan forgiveness? What to do

Here’s how much people really tip

While this means you’ll pay taxes up front, your money will grow free of taxes in the Roth 401(k). You’ll also be able to take tax-free withdrawals in retirement.

Separately, advisors like that entrepreneurs have the option of taking a loan from a solo 401(k) if it’s necessary. You can’t do that with an IRA.

SEP IRA. Employers are limited to contributions of either 25% of the employee’s compensation or $56,000 for 2019.

Elective salary deferrals by employees and catch-up contributions for people aged 50 and up aren’t allowed. SEP IRAs are funded only by the employer.

From a business owner’s point of view, SEPs are cheap and easy to manage, said Pottichen.

Be sure to consider the cost and the flexibility of the plans when you work with your CPA or advisor to decide.

“With a self-employed 401(k), you might have some administrative costs you won’t see with the SEP IRA,” said Pottichen. “But there’s also a lot of flexibility with the self-employed 401(k).”