Kenneth Fisher, chief executive officer of Fisher Investments, speaks at the Forbes Global CEO Conference in Sydney, Australia, on Tuesday, Sept. 28, 2010.

Gillianne Tedder | Bloomberg | Getty Images

It remains to be seen how long other clients will stick with billionaire money manager Ken Fisher in the wake of off-color and sexist comments he recently made at an investing conference.

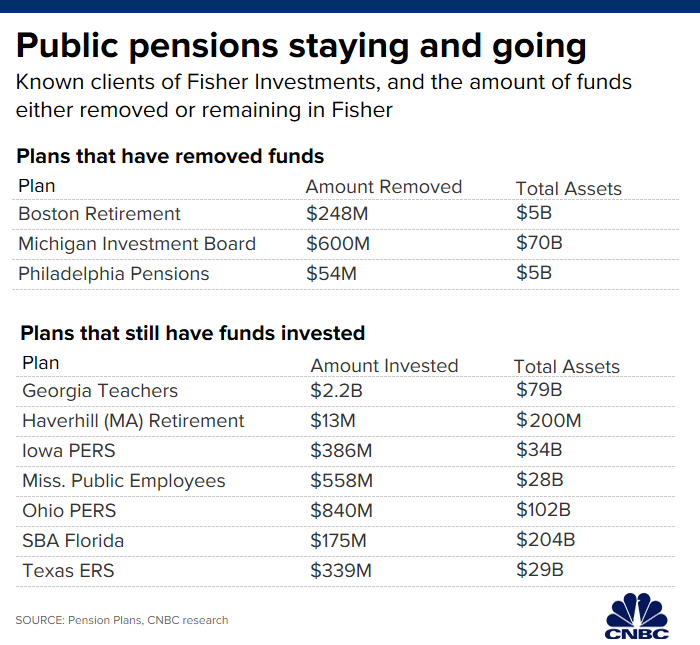

Close to $1 billion in public pension assets have left Camas, Washington-based Fisher Investments so far, including the Boston Retirement System with $248 million in assets and $600 million the State of Michigan says it’s withdrawing.

Philadelphia’s board of pensions also said it would move the $54 million it has with Fisher.

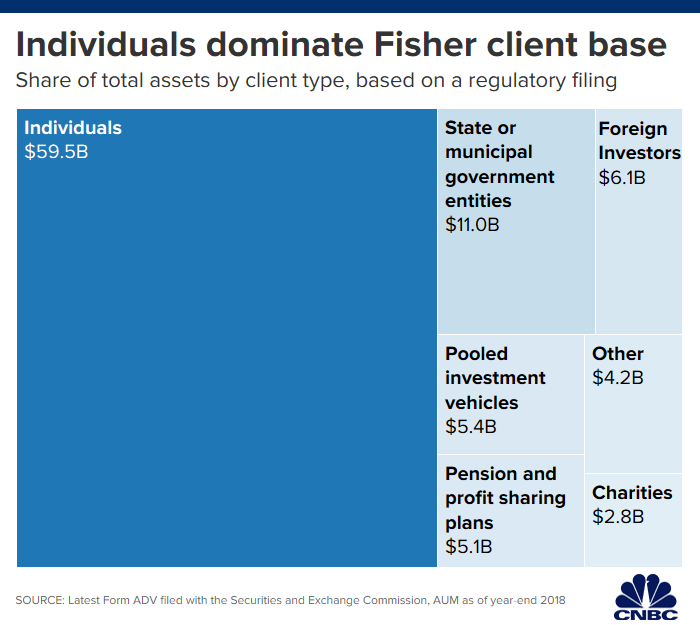

While government-run pension funds make up a relatively small amount of the overall assets managed at Fisher Investments, $10.9 billion from 36 entities, according to the firm’s regulatory filing with the Securities and Exchange Commission, how they respond may be a bellwether for other clients of the firm, industry experts say.

In all, Fisher had $94 billion in assets under management as of Dec. 31, 2018, according to their SEC filing. That figure reached $112 billion as of Sept. 30, 2019, according to the firm.

The speed with which pensions moved assets from the money manager surprised even attorneys who specialize in retirement plans.

That’s because these plans normally take two to three quarters to decide whether they want to change investment advisors, said George Michael Gerstein, an attorney at Stradley Ronon in Washington, D.C.

“I typically caution plan fiduciaries against acting too hastily in deciding whether to fire or hire or offer a new investment option to participants,” he said.

Who remains

The spate of divestitures was spurred by sexist comments Fisher made at the Tiburon CEO Summit on Oct. 8 — which public officials also cited as a reason for firing his firm.

Fisher has since apologized for his comments.

“Some of the words and phrases I used during a recent conference to make certain points were clearly wrong and I shouldn’t have made them,” he said in a prepared statement. “I realize this kind of language has no place in our company or industry. I sincerely apologize.”

While individual investors can pick up their assets and go at any time, retirement plans tend to proceed deliberately, even if they’re investing their funds with an array of managers.

This could be why other plans aren’t yet rushing for the exits at Fisher.

Indeed, the State Board of Administration of Florida, which has a $175 million relationship with the firm, has been in contact with Fisher Investments and is performing its due diligence, said John Kuczwanski, a spokesman for the plan.

Further, the Haverhill Massachusetts Retirement System, which has about $200 million in total assets, expects to address its next steps in an upcoming board meeting in November.

“It’s up for discussion,” said administrator David Van Dam. The Haverhill pension plan has $13 million invested with Fisher.

Public retirement plans are subject to state law, and the boards that govern them are fiduciaries — even though the federal laws that apply to corporate 401(k) plans don’t apply to them.

This means the pension plans must act in the best interest of their beneficiaries and participants, and they must back their decisions with the appropriate due diligence.

“There are a lot of quantitative and qualitative factors that are reviewed before deciding to remove someone,” said Marcia Wagner, founder of The Wagner Law Group in Boston. “It isn’t a snap decision.”

Prudent process

Hinterhaus Productions | The Image Bank | Getty Images

The research plan fiduciaries undertake before firing an investment manager include analyzing fees and performance and determining how that manager fits within the overall asset mix at the plan, said Wagner.

Plan fiduciaries are also responsible for considering whether a move could hurt beneficiaries either in the form of higher costs or a reduction in service, said Bradford Campbell, partner at Drinker Biddle in Washington, DC.

A plan could put a service provider on a watch list for several quarters while undergoing the appropriate research, Gerstein said.

More from Personal Finance:

Ken Fisher’s sexist comments have cost his firm nearly $1 billion

Millennials aren’t counting on Social Security in retirement

Road trip: 10 global hotspots

“There is a duty to continually monitor the prudence of service providers to make sure they are serving the plan’s interest,” he said. “It’s not a ‘set it and forget it’ decision.”

While it may be out of character for a pension plan to drop an investment advisor in a matter of days, this latest development could be a sign that plan fiduciaries are becoming socially conscious — and that’s at least one factor in their decisions.

“People are people, and if they find something to be truly obnoxious, they will vote with their feet,” said Wagner.

CNBC’s Elly Cosgrove, Jessica Dickler and Will Feuer contributed to this report.