Stock market down on coronavirus fears.

Getty

Worldwide, more than 4,000 deaths. More than 120,000 infected. Cratering stock prices. Plunging interest rates. Plummeting oil prices. Supply chains, stressed by tariffs, now broken. Necessities stripped from store shelves. Quarantines. Social distancing. Mall traffic tumbling. Restaurants struggling. Flights canceled. Conferences canceled. March Madness now sadness. Business and consumer confidence shaken.

There’s something happening here. What it is ain’t exactly clear. But here are a few things we do know:

- The looming recession is worldwide. It is a demand- and supply-side recession that necessitates demand- and supply-side responses.

- Demand-side macroeconomic policy entails getting consumers and business to spend more. These policies are textbook responses that don’t vary from recession to recession. Policymakers will choose from off-the-shelf proposals. Monetary (demand-side) stimulus is only mildly helpful in the current situation. The positive impact of further rate cuts is limited. The ability to cut rates (because they are already approaching zero) is limited. This time the gridlocked Congress cannot depend on the Federal Reserve to provide anti-recession medicine. (But the Fed still has an important role on the supply side. See below.)

- Echoing the views of macroeconomists worldwide, European Central Bank President Christine Lagarde said March 12: “An ambitious and coordinated fiscal policy response is required to support businesses and workers at risk.”

- As in prior recessions, targeting tax cuts and government spending programs to lower-income households would provide the largest stimulus because their propensity to spend is larger. Fiscal assistance from the federal government to state and local governments would allow them to maintain spending. To spur business spending, Congress might consider a temporary investment tax credit or superdeduction for capital expenditures.

- Historically, timing is always a problem with fiscal stimulus. Action almost always is late. It takes a while to recognize the problem. It then takes a while for Congress to act. And then it takes a while for proposals to take effect. For example, many spending programs are not “shovel ready.”

- It seems clear that negative demand-side effects will be large. But how large? That remains a mystery. Data aren’t yet available. Without a reading of the magnitude of the effect of the coronavirus on GDP, it will be difficult for economists to prescribe the size of the fiscal stimulus package needed. For example, if GDP declines by 5 percent (about $1 trillion), macroeconomists might recommend an increase in government spending of $500 billion, given that they assume a policy multiplier of 2.

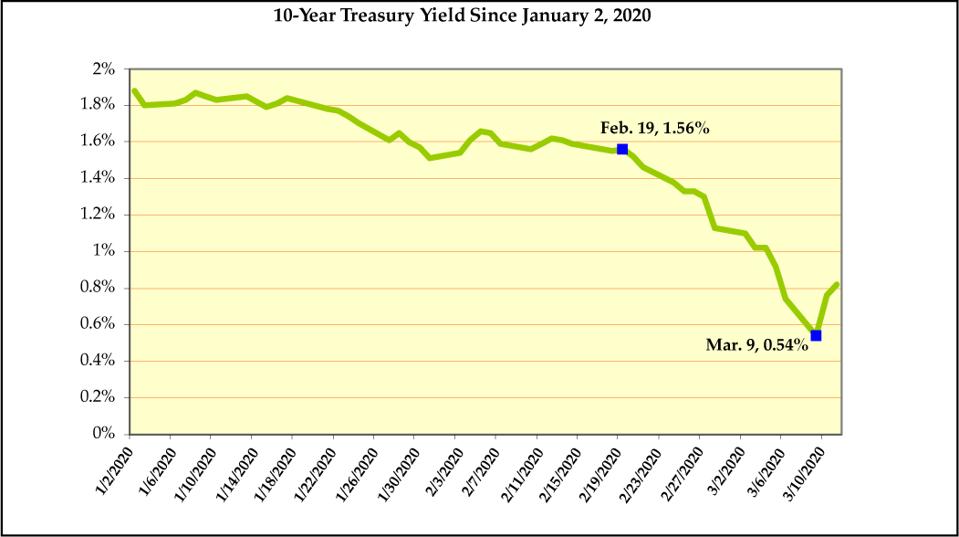

- This is no time to be a deficit hawk. The United States still has tremendous borrowing capacity, and this is exactly the time to use it. Also, note well: Plummeting interest rates already are working to reduce the size of federal interest costs and, therefore, of the federal deficit. (See the figure showing 10-year Treasury yields.) But the need for fiscal restraint will be greater than ever after the crisis has passed.

- Because of worldwide slowdown, demand for U.S. exports will decline. Further, because of “flight to safety,” there will be an increase in the demand for U.S. securities and, along with it, an increase in the demand for the dollar. The resulting appreciation of the dollar will further dampen demand for U.S. exports. Perhaps this isn’t a good time to engage in a trade war.

- Supply-side policy entails maintaining the productive capacity of the economy. These policies need to be directed at supply shocks that are threatening. Solutions tailored to the current situation are required.

- Health. Government support for coronavirus mitigation measures — testing, treatment, vaccines, public education — directs resources to the root cause of the current economic problems and therefore is a well-targeted supply-side response. To the extent this entails more government spending, it also provides demand-side stimulus.

- Workforce. It’s unclear that anything can be done about broken supply chains attributable to foreign manufacturing slowdowns (for example, in China and Italy). However, domestic supply disruptions attributable to unprecedented workforce disruptions need situation-specific responses. For example, with schools closing, what can be done to keep working parents working? Do teleworking policies (of business and government) need to be reappraised?

- Cash and credit (1). If customers aren’t buying, businesses immediately face cash flow problems. For large businesses, this issue is exacerbated by the recent binge of borrowing at low rates. Large businesses are now making a dash for cash — tapping their existing lines of credit. But far more problematic is the liquidity crunch faced by small- and medium-size businesses. Here is where Fed policies can have a major impact: targeting and guaranteeing credit flows from banks to small- and medium-size businesses.

- Cash and credit (2). There’s a moral hazard problem of bailing out financially weakened borrowers. But this problem of creating an incentive for imprudent risk-taking must be weighed against the huge out-of-pocket and long-term economic costs of widespread business bankruptcy.

- Cash and credit (3). Unlike 2008, this economic downturn didn’t start in credit markets. But the Fed must be alert to possibilities that this health issue may create unprecedented financial stresses (for example, margin calls that require forced selling).

- Although equity futures took a dive after President Trump’s March 11 “foreign virus” speech, his proposals for the Small Business Administration to extend loan guarantees for business borrowing and for Treasury to postpone some tax payments without penalties deserve high marks. Businesses need cash. And the federal government has the power to get it to them.

- With confidence low and uncertainty high, the mere act of signaling that credible and effective anti-recession macroeconomic policies will be enacted in the future can have an immediate positive benefit. The cry for policymakers fighting this battle: “Whatever it takes!”

10-Year Treasury Yield Since January 2, 2020

Martin Sullivan

This article was originally published by Forbes.com. Read the original article here.