I will pay my taxes sentence written repeatedly on blackboard as a punishment.

Getty

Routine activity theory explains tax evasion by looking at it as the convergence of motivated taxpayers, attractive tax savings, and guardians that are incapable of stopping or deterring evasion. Greater tax burdens and heavy reliance on self-assessment facilitate an environment conducive to evasion.

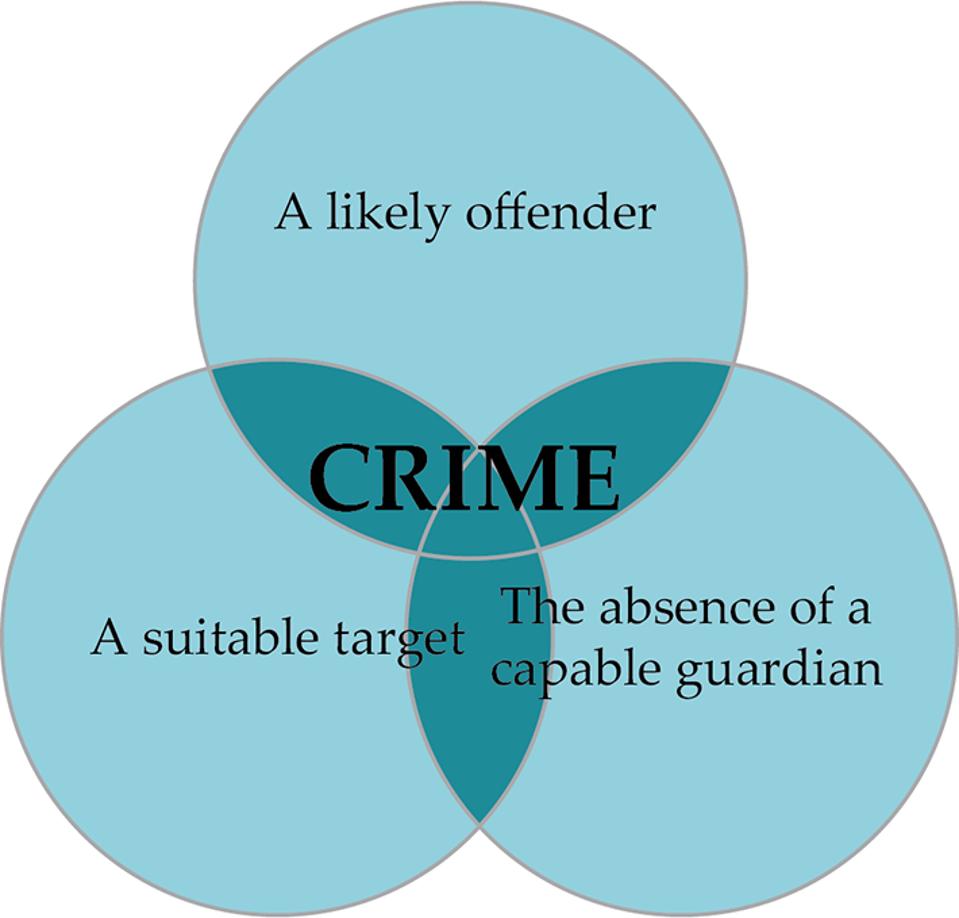

According to routine activity theory, crime occurs when three conditions converge: a motivated offender, an attractive target, and the absence of a guardian. Being able to commit a crime is not enough; motivated offenders must also be willing to do so. Suitable targets are attractive and vulnerable. Guardians are persons or objects that stop or deter offenses.

Examples of guardians include a perpetrator’s handler or a target’s protector. Superguardians regulate guardians, and they can include external parties. In the tax arena, guardians and superguardians include tax advisers, auditors, and the IRS. Professional ethics and licensing requirements guard the guardians.

Venn diagram of a crime.

Carrie Brandon Elliott

Marcus Felson and Lawrence Cohen created routine activity theory to explain U.S. crime rate changes between 1947 and 1974. Routine activity theory assumes that crime is unaffected by social conditions like poverty, inequality, and unemployment. In fact, prosperity creates more opportunity for crime to occur, explaining why crime rose after World War II when Western economies and welfare states were growing. In other words, crime is a function of opportunity that doesn’t require dangerous or evil people. If a target is unprotected and worth the reward, crime will occur. Most crime is mundane, petty, and unreported.

Unlike criminology, routine activity theory studies crime in relation to its environment, avoiding speculation about offender motivation. This makes it useful for explaining — and, therefore, for deterring — instrumental crimes like tax evasion that involve planning and risk assessment (as opposed to expressive crimes involving emotion). Part of the goal of routine activity theory is to enable situational crime prevention, meaning measures that attempt to manage, design, or manipulate the environment to reduce the opportunity for crime by making it more risky or less rewarding.

According to routine activity theory, tax evasion is inevitable and mostly undetected. There will always be taxpayers who seek to generate tax savings through evasion; speculating about offender motivations is unproductive. Tax savings are an inherently attractive target that becomes more attractive the higher the tax liability. Reducing the tax burden arguably makes tax evasion less rewarding.

A target’s vulnerability depends on guardian capability. The target is more vulnerable — and thus tax evasion is more likely — in complex or opaque tax systems with inadequate audit or enforcement functions. Measures like tax simplification and information sharing can be viewed as situational crime prevention; they make tax evasion more difficult and riskier for potential offenders. These same measures, along with disincentives for collaborating with offenders, yield capable guardians and superguardians.